.svg)

.svg)

Accounts and Cards Support

Browse Accounts and Cards Topics

Certificates & IRAs

Find answers about Keesler Federal certificates and IRA accounts, including rates, terms, and account management.

If the withdrawal does not reduce the certificate funds below the required minimum balance for this type of certificate, the member shall forfeit at the certificate rate an amount equal to the lesser of:

All dividends for 90 days from the amount withdrawn for certificates with a term of 1 year or less; or all dividends for 180 days on the amount withdrawn for certificates greater than 1 year; or all dividends on the amount withdrawn since date of issuance or renewal.

If the amount withdrawn reduces the certificate funds below the required minimum balance for this type of certificate, the entire certificate will be canceled and the member shall forfeit at the certificate rate an amount equal to the lesser of:

All dividends for 90 days on the entire amount of the certificate if the certificate is for a term of 1 year or less; or all dividends for 180 days on the entire amount of the certificate if the certificate is for a term of 1 year or more; or all dividends on the entire certificate since the date of issuance or renewal.

Contributions cannot be totaled for a prior tax year because IRA contributions can be accepted for a prior tax year from Jan. 1-April 15. It is the member’s responsibility to know what they have contributed for the tax year they are filing their income tax return.

This is the Required Minimum Distribution for any Traditional IRA members that have reached the age of 73 (as of January 1, 2023). The IRS requires Traditional IRA owners to take a set amount out of their IRA’s each year once they reach 73. This figure is calculated from their prior year ending balance in their IRA on Dec. 31 and their age divisor from the IRS Uniform Lifetime Table. Their amount will vary each year based on their balance changing each year and their age divisor changing each year.

This is the tax document that reflects any contributions they have made for a prior tax year; members receive this in mid-May of the following tax year.

This is the IRA tax document the member will receive in early February reflecting the amount they took out of their IRA for a prior tax year.

The member can request by signed fax, message board, or by visiting a FSR at any branch. If they are requesting by fax, or message board they will need to include in the request if it is a distribution from their Traditional IRA if they would like any federal taxes withheld and include the percentage (this will need to be 10% or greater) -OR- they can opt to state “ they do not want any taxes withheld” They will also need to include the amount to withdraw and how they want to receive the funds, ex. Deposit to savings, checking, HIMMA, or mail check.

If the member is only taking a distribution of their contribution amount they will not be assessed an early withdrawal penalty. However, if they are removing any dividends prior to the age of 59 ½ they would be subject to a 10% early withdrawal penalty and taxes on the dividends earned only. This usually only comes into play if the member is taking a full distribution of their Roth IRA funds.

If the member is under the age of 59 ½ and they withdraw from their Traditional IRA they will be liable for the 10% early withdrawal penalty in addition to any taxes they may owe based on their tax bracket. We are not able to determine what their tax liability may be since everyone’s income tax bracket is different.

If the member is over age of 59 ½ and they withdraw from their Traditional IRA there is no early withdrawal penalty.

No, as long as you are working and have reportable income you can contribute up to the maximum allowable each year as long as it does not exceed what you have earned for the year.

You can contribute to both a Traditional and Roth IRA at any age as long as you are still working and have earned income.

No, you are not eligible to make contributions if you no longer have earned income. Social Security, Disability, or Retirement income do not qualify as earned income.

*If you are unsure if you are eligible to contribute you should speak to your tax preparer for guidance.

The maximum allowable to contribute to an IRA or aggregate of all IRAs for 2026 is:

$7,500 under age 49 or less

$8,600 age 50 and older

*Earned income of at least the amount that you want to contribute is required by the IRS. If you are unsure what you are eligible to contribute you should speak to your tax preparer for guidance.

$0, there is no minimum amount to open an IRA.

Traditional IRA contributions “may” be tax deductible. Roth IRA contributions are normally made with after tax dollars. Please seek advise from your tax preparer to know which one is best for you.

Checking Accounts

Get help with Keesler Federal checking accounts, including account features, services, and managing your account.

No. To open a checking account, members are required to have a savings share account with a minimum $5 balance at all times.

Yes, each debit card linked to your checking account must have the same Smart Change status.

During business hours, call Keesler Federal. After hours, use the listed card activation, PIN change, lost or stolen card, or fraud alert numbers depending on card type and need.

- Customer Service New Phone Number: 888-533-7537

- Lost/Stolen Cards New Phone Number: 800-315-3046

- Change/Reset PIN New Phone Number: 888-886-0083

- Card Activation New Phone Number: 800-631-3197

Each debit card purchase will still appear on your account for the actual amount of the transaction. At the end of each business day, one Smart Change transfer will be made for the total of the rounded up difference for each of your debit card purchases posted on that day. This transfer will appear as on your account as a single line item transaction.

Example:

Day 1 Debit Purchase: Gas $28.15

Day 1 Debit Purchase: Grocery $55.48

Day 1 Debit Purchase: Amazon $44.75

Day 1 Smart Change Transfer to Savings: $1.62 (.85 +.52 +.25)

If your account balance is insufficient to cover the entire amount of your automatic Smart Change transfer, we will only transfer the amount of funds up to a $0.00 (zero) balance.

Example: Your checking account balance is $1.00. Your round up funds for that day totals $1.50. In this case, Smart Change will only transfer $1.00 to your Smart Change savings account. If your account has a negative balance, the entire Smart Change transfer for that day will be skipped.

NOTE: There are no “catch up” transfers for skipped transactions due to an insufficient balance. Transfers can only occur on the same day that your debit card purchases post. Please also be aware that although your Smart Change transfer amount will be adjusted (or skipped) for an insufficient or negative balance, your actual purchase amount will still post even if it results in an overdraft on your account.

Yes, you may make up to 6 withdrawals per month through online and mobile banking or by calling or visiting a branch.

You can order checks online, by calling our Member Contact Center or visiting a branch. You will need your routing number, account number, and zip code.

The debit card you ordered during the sign up process should arrive in 7-10 days. Once you have activated it, be sure to add it your preferred digital wallet.

No. Smart Change savings accounts can only receive funds via automatic system transfers resulting from your debit card purchases.

Credit Cards

Once you activate your new Visa card, the balance on your existing credit card will automatically transfer to the new Visa account. This balance will continue to accrue interest at your pre-existing interest rate until it is paid in full. New purchases made with your Visa card will be subject to the rate of your new Visa card.

Want to take advantage of Keesler Federal’s low rates? You can transfer up to your Keesler Federal credit card limit from another credit card. The best part? We don’t charge any balance transfer fees!

You can transfer up to your Keesler Federal credit card limit from another credit card with no balance transfer fees. Fill out our Balance Transfer form to get started.

The payments for credit card accounts are calculated at 3% of the balance plus any over limit amount. Credit Life and Credit Disability is calculated and added each month based on the balance of the account at the time statements run.

- Late fee: Up to $25.00 after payment is 10 days late

- Returned Item fee: $25.00 per return item

- Cash Advance: $ 5.00

- Credit Card Statement: $2.00

- Credit Card Convenience Check Stop Pay Fee: $25.00 per request

Up to $100,000.

The APR will be determined by the risk score assigned to the credit report pulled at the time the loan application is processed.

Due to the different disclosures for each card, the members who wish to convert to a new card type must sign a new application. Once the new account is opened, the balance on the existing credit card account will be transferred to the new card.

Your new Visa card will have a different card number and expiration date. Therefore, if your old Keesler Federal credit card is on file with any merchants for recurring payments (e.g.: mobile phone/internet service, Amazon, Netflix, PayPal, etc.), please remember to update those accounts with your new card information.

Savings Accounts

Learn how Keesler Federal savings accounts work and get help managing your account.

No, members are not required to have any other accounts to open a savings account. However, to open a checking account, members are required to have a savings share account with a minimum of $5 at all times, which can be utilized as a savings account.

Yes, you may suspend your participation in Smart Change at any time by calling us or visiting any branch. The change will take effect on the same day. Funds already accumulated will remain in your Smart Change account and continue to earn 2% in dividends until you opt to withdraw or transfer those funds out. If the checking account is closed, the Smart Change account will close and the funds will be moved into your primary share.

Minimum $5.00 deposit to open. Keesler Federal will deposit the first $5.00 for all new members up to 12 months of age.

Primary share ID is 0001. Minimum $5.00 deposit to open. Keesler Federal will deposit the first $5.00 for all new members up to 12 months of age.

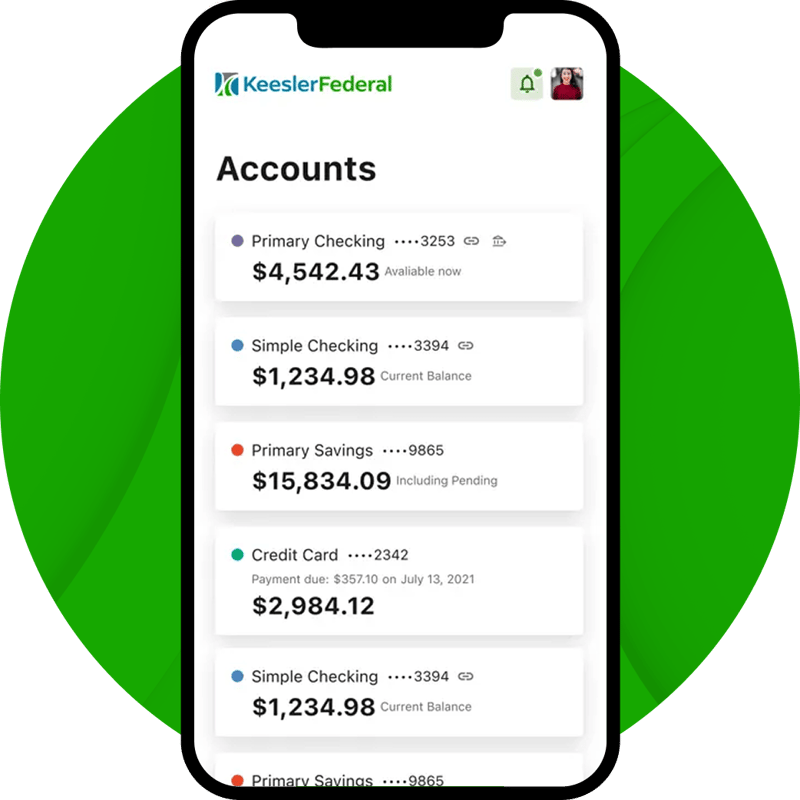

Bank Anytime with the Keesler Federal Mobile App

The Keesler Federal Mobile Banking App lets members securely access accounts, deposit checks, transfer funds, and track everyday spending directly from their phone.

- Securely check balances, move money, and deposit checks from anywhere

- Deposit checks, pay bills, and send money quickly using secure mobile banking tools

- Set up account alerts and track spending to stay in control of your finances

.svg)